The Union Minister of Finance and Corporate Affairs Smt. Nirmala Sitharaman presented the Union Budget 2024-25 in Parliament today. The highlights of the budget part-B are as follows:

Indirect Taxes

GST

- Buoyed by GST’s success, tax structure to be simplified and rationalised to expand GST to remaining sectors.

Sector specific customs duty proposals

Medicines and Medical Equipment

- Three cancer drugs namely TrastuzumabDeruxtecan, Osimertinib and Durvalumab fully exempted from custom duty.

- Changes in Basic Customs Duty (BCD) on x-ray tubes & flat panel detectors for use in medical x-ray machines under the Phased Manufacturing Programme.

Mobile Phone and Related Parts

- BCD on mobile phone, mobile Printed Circuit Board Assembly (PCBA) and mobile charger reduced to 15 per cent.

Precious Metals

- Customs duties on gold and silver reduced to 6 per cent and that on platinum to 6.4 per cent.

Other Metals

- BCD removed on ferro nickel and blister copper.

- BCD removed on ferrous scrap and nickel cathode.

- Concessional BCD of 2.5 per cent on copper scrap.

Electronics

- BCD removed, subject to conditions, on oxygen free copper for manufacture of resistors.

Chemicals and Petrochemicals

- BCD on ammonium nitrate increased from 7.5 to 10 per cent.

Plastics

- BCD on PVC flex banners increased from 10 to 25 per cent.

Telecommunication Equipment

- BCD increased from 10 to 15 per cent on PCBA of specified telecom equipment.

Trade facilitation

- For promotion of domestic aviation and boat & ship MRO, time period for export of goods imported for repairs extended from six months to one year.

- Time-limit for re-import of goods for repairs under warranty extended from three to five years.

Critical Minerals

- 25 critical minerals fully exempted from customs duties.

- BCD on two critical minerals reduced.

Solar Energy

- Capital goods for use in manufacture of solar cells and panels exempted from customs duty.

Marine products

- BCD on certain broodstock, polychaete worms, shrimp and fish feed reduced to 5 per cent.

- Various inputs for manufacture of shrimp and fish feed exempted from customs duty.

Leather and Textile

- BCD reduced on real down filling material from duck or goose.

- BCD reduced, subject to conditions, on methylene diphenyl diisocyanate (MDI) for manufacture of spandex yarn from 7.5 to 5 per cent.

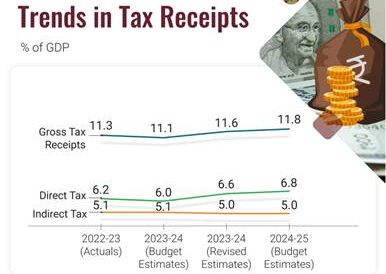

Direct Taxes

- Efforts to simplify taxes, improve tax payer services, provide tax certainty and reduce litigation to be continued.

- Enhance revenues for funding development and welfare schemes of government.

- 58 per cent of corporate tax from simplified tax regime in FY23, more than two-thirds taxpayers availed simplified tax regime for personal income tax in FY 24.

Simplification for Charities and of TDS

- Two tax exemption regimes for charities to be merged into one.

- 5 per cent TDS rate on many payments merged into 2 per cent TDS rate.

- 20 per cent TDS rate on repurchase of units by mutual funds or UTI withdrawn.

- TDS rate on e-commerce operators reduced from one to 0.1 per cent.

- Delay for payment of TDS up to due date of filing statement decriminalized.

Simplification of Reassessment

- Assessment can be reopened beyond three years upto five years from the end of Assessment Year only if the escaped income is ₹ 50 lakh or more.

- In search cases, time limit reduced from ten to six years before the year of search.

Simplification and Rationalisation of Capital Gains

- Short term gains on certain financial assets to attract a tax rate of 20 per cent.

- Long term gains on all financial and non-financial assets to attract a tax rate of 12.5 per cent.

- Exemption limit of capital gains on certain financial assets increased to ₹ 1.25 lakh per year.

Tax Payer Services

- All remaining services of Customs and Income Tax including rectification and order giving effect to appellate orders to be digitalized over the next two years.

Litigation and Appeals

- ‘Vivad Se Vishwas Scheme, 2024’ for resolution of income tax disputes pending in appeal.

- Monetary limits for filing direct taxes, excise and service tax related appeals in Tax Tribunals, High Courts and Supreme Court increased to ₹60 lakh, ₹2 crore and ₹5 crore respectively.

- Safe harbour rules expanded to reduce litigation and provide certainty in international taxation.

Employment and Investment

- Angel tax for all classes of investors abolished to bolster start-up eco-system,.

- Simpler tax regime for foreign shipping companies operating domestic cruises to promote cruise tourism in India.

- Safe harbour rates for foreign mining companies selling raw diamonds in the country.

- Corporate tax rate on foreign companies reduced from 40 to 35 per cent.

Deepening tax base

- Security Transactions Tax on futures and options of securities increased to 0.02 per cent and 0.1 per cent respectively.

- Income received on buy back of shares in the hands of recipient to be taxed.

Social Security Benefits.

- Deduction of expenditure by employers towards NPS to be increased from 10 to 14 per cent of the employee’s salary.

- Non-reporting of small movable foreign assets up to ₹20 lakh de-penalised.

Other major proposal in Finance Bill

- Equalization levy of 2 per cent withdrawn.

Changes in Personal Income Tax under new tax regime

- Standard deduction for salaried employees increased from ₹50,000 to ₹75,000.

- Deduction on family pension for pensioners enhanced from ₹15,000/- to ₹25,000/-

- Revised tax rate structure:

| 0-3 lakh rupees | Nil |

| 3-7 lakh rupees | 5 per cent |

| 7-10 lakh rupees | 10 per cent |

| 10-12 lakh rupees | 15 per cent |

| 12-15 lakh rupees | 20 per cent |

| Above 15 lakh rupees | 30 per cent |

- Salaried employee in the new tax regime stands to save up to ₹ 17,500/- in income tax.